How I Underwrite MCA Participations From a Pool

- Ali Barkhordar

- Jul 8

- 2 min read

A merchant cash advance is not a loan. It is a purchase of future receivables at a discount, remitted from daily sales. When I participate in a pool of these positions rather than originate them myself, my entire edge reduces to one thing: which deals I say yes to.

Most participants sort by yield. I think that is backwards. Yield is the compensation for risk you have already accepted, not a reason to accept it. The work that decides the outcome happens before yield enters the conversation.

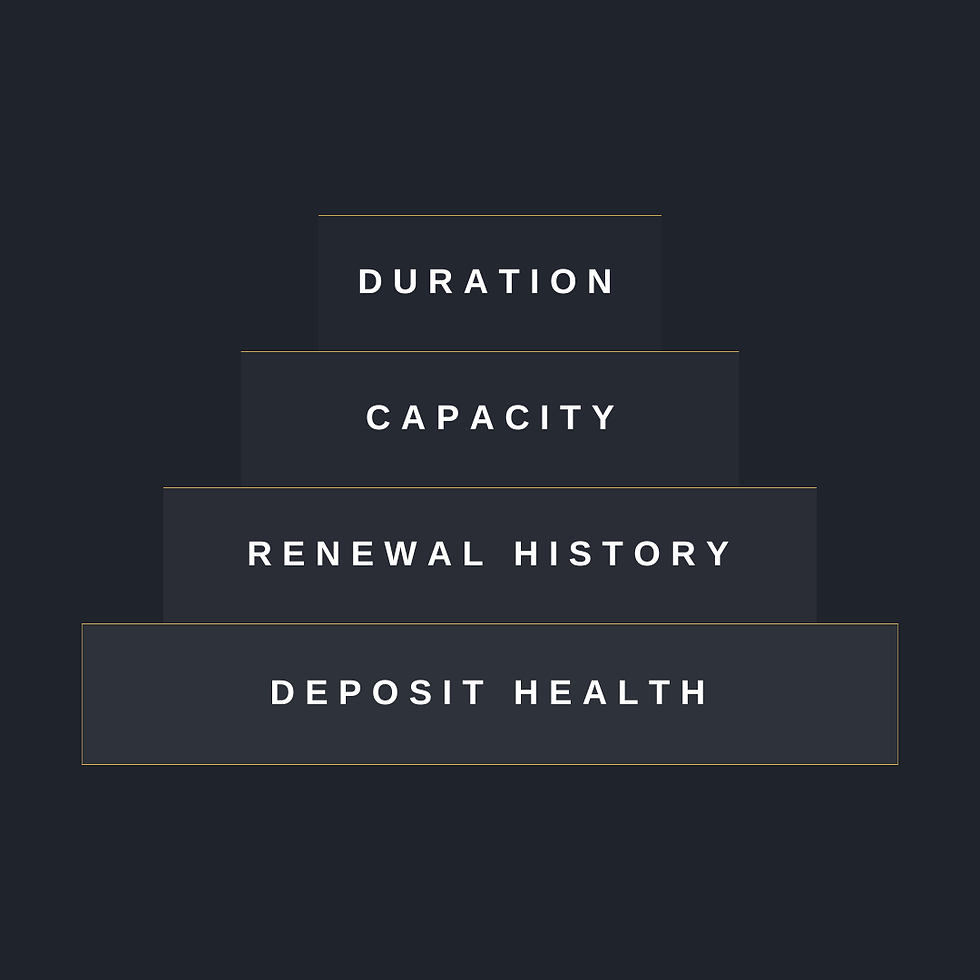

My MCA Participation Underwriting Order

Duration comes first. Expected term is the cleanest proxy I have for uncertainty. Every additional week of remittance is another week of exposure to events no funding tape can show me. Shorter is not a preference, it is a discipline that caps what I cannot forecast.

Capacity comes second. I ask whether the daily remittance leaves the merchant enough working capital to keep operating. A position that starves the business does not get repaid on schedule, no matter how the receivables purchase looks on paper.

Renewal history comes third. A merchant who has retired a prior position and come back has told me something no credit model can: how they behave under an actual obligation. That outranks any prediction of it.

Deposit health comes last, and it confirms everything above. Average daily balance, ending balances, NSF cadence. That is the ground truth. Every factor before it is either validated or contradicted in the bank record.

Sorting by yield asks what a deal pays me. My order asks whether it pays me at all. Only one of those questions gets to be answered first.

I wrote up the same framework in more formal terms on the Ultimate Business Capital blog, if you want the institutional version: MCA participation underwriting.